The Securities Transaction Tax (STT) has long been a flashpoint among traders in India—the consensus among many is that STT makes participating expensive and distorts market behaviour and operations. In one way or another, Nithin Kamath, co-founder of Zerodha, has been one of the loudest advocates for change here. He believes that given the current trading tax structure, volumes disproportionately flow in certain instruments – primarily options – while discouraging any action in cash equities and futures.

Nithin Kamath’s Perspective on STT

Kamath’s critique of STT stems from its cost structure, trader behaviours, and the equilibrium of markets as a whole. He makes arguments based on the premise that while transaction taxes are enacted to generate revenue and control market activity, they also create negative distortions that naturally limit efficiency.

Concerns About STT As Compared To Brokerage

One of Kamath’s primary concerns is that STT exceeds brokerage for many trades. Zerodha’s model already offers low or zero brokerage in many segments. However, the STT burden can be an added hindrance for traders, particularly for retail traders. They may perceive STT as an additional cost, leading to reduced returns and fewer trades.

Kamath also argues that the way STT is disclosed to traders is convoluted. A single transaction may involve several charges, including brokerage, exchange costs, STT, and any other incidental levies, which can hide the real cost of each charge. Removing or at least reducing STT would reduce the way costs are disclosed to traders and make cost disclosure clearer.

Effects on Trader Behaviour

High transaction taxes can change how traders behave. Kamath argues that STT alters behaviours about frequent, or intraday, trades in segments such as cash equities and futures; the result is less liquidity in the market. When there is less liquidity in the market, price discovery is negatively impacted since fewer trades allow less real-time information to determine asset valuations.

Additionally, when trading costs are higher, smaller traders will inevitably pull back, or even stop trading, which results in the larger institutional traders dominating the segment. Kamath characterises the changes to STT as a move toward encouraging a wider population of traders by type of trader to participate in the market.

Public Advocacy and Awareness

Kamath uses social media and public forums as methods to promote awareness of STT. He actively joins conversations on Twitter and through forums such as Zerodha Online to engage both experts on the topic and the everyday traders and discuss the role of STT in shaping behaviour in the market. All his arguments are data-based, but Kamath’s advocacy has added a larger platform to discuss the need for changes in India’s cost structure for the market.

Effects of the Securities Transaction Tax on Indian Markets

The way STT is levied has demonstrated a clear association with how traders make choices of cash equities, derivatives, or other financial equities. Changes to the application of STT over the years have created clear shifts in volumes.

Its Direct Impact on Trading Volumes

STT is a direct tax on each buy and sell transaction and increases the cost of execution on every trade. Kamath points out that in many cases STT is more than the brokerage fee charged, especially for high-frequency or intra-day transactions, and adds a deterrent for traders to execute multiple trades in one session — reducing liquidity.

When STT gets reduced, trading activity typically increases as costs have become less prohibitive, especially for intra-day trades where your margins are thin and leverage critical.

Movement to Options Trading

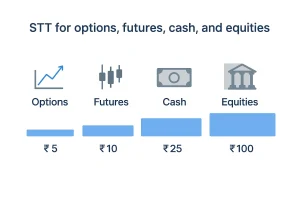

Perhaps a prime contributor to the rapid growth of options trading in India is how STT taxes are levied. For options, the tax is implemented only on the premium amount – not the full contract value. In the futures and cash equity segment, the tax is imposed on the whole trade value, thus making it significantly more expensive than options trading.

This difference has made options a very attractive form of trading for anyone looking to reduce their costs. The pricing of options has become more appealing to traders and, over time, has reduced activity in other segments like futures and cash equities in favour of options.

| Instrument | STT Calculation Basis | Effect on Trading Cost |

| Options | Premium value | Lower relative cost |

| Futures | Contract value | Higher relative cost |

| Cash Equity | Total trade value | Moderate cost |

In the past, it wasn’t always this way. Before 2008, STT on options was on the full contract value. This made them way less attractive than plain shares. Once they changed to taxing the premium value, they became popular.

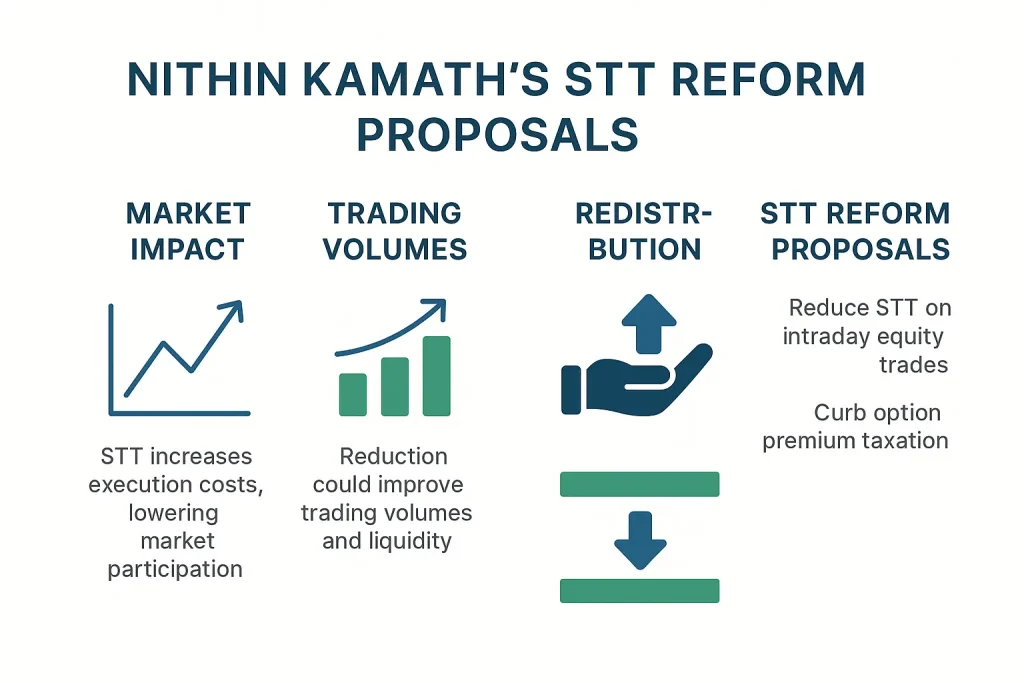

Policy Suggestions and Market Reforms

Kamath’s proposals centre on two main levers: STT on cash equities and futures and intraday leverage limits. In his view, these changes could help redistribute volumes across product types to create a healthier ecosystem.

Lowering STT on Cash and Futures

Lowering STT in these segments would lower trading costs, encouraging increased participation. STT is applied to the total transaction value, so the effect is magnified on high-value trades. Lowering costs to better align with brokerage fees will allow cash equities and futures markets to compete with options.

Adjusting Intraday Leverage

Kamath also suggested increasing intraday leverage for cash equities and futures, which is also currently limited, often around 20%. This can be political, and the difficulty of every single product is in making sure the market does not see it as moving toward trivialising more risky behaviour. If intraday leverage is at least more closely aligned with / or improved in cash equities and futures, it opens in interest-weighted to the liking as applied in the financing of them leveraged trades seen in other markets.

Balancing Volume & Growth

By lowering the costs associated with cash and futures and improving available leverage, regulators are able to rein in the level of concentration of swelling, growing activity in options. The proliferation of this will dull the volume found across the other products. Distributing /and balancing trade flow across products promises to enhance market stability and liquidity potential.

Broader Implications for Brokers and Market Participants

Zerodha’s stance on STT reform encapsulates its perspective as a low-cost, tech-driven broker. It has already disrupted the brokerage space with its pricing, and this call for reform aligns perfectly with what their aim is: to reduce both the time and costs for any trader.

Others in the brokerage space may be pressured to also step in to advocate for lower costs to keep their clients, and also to stay competitive on value. If regulators took action on these calls to reform STT, the effects would be felt, not only by the individual traders but also around the efficiencies of capital markets in India.

The Role of Trading Tax Reform in the Bigger Picture

Changing the policy around trading tax will be more than just saving the trader money. It will create a healthier market. By minimising distortions around product choice and encouraging a more uniform distribution of activity, policymakers could promote deeper liquidity and better price discovery.

These reforms could also help increase participation from less sophisticated, smaller investors, who may be inhibited by comparatively higher costs. If cash, for example, is attractive, futures and options will be attractive as well. A well-balanced market with cash, futures, and options all being active together is more resilient and better able to absorb shocks.

Conclusion: Lower Costs, Healthier Markets

Discussion on STT reform isn’t winding down. Nithin Kamath is clear; while abolishing the tax may be unrealistic, he advocates recalibrating rates and structure to help establish a more balanced market. Lower costs in cash equities and futures, with competitive leverage, have a chance to swing volumes back from options and enable broad-based participation.

Traders’ understanding of their position versus STT across different segments is vital for informed decision-making. And as for access to low-cost, low-effort methods to participate in the market, other companies like Marketbhai provide tools, resources, and transparent pricing that traders can access. Strategic alignment with both cost structure and market structure means traders can work towards a better result, where ultimately, it lands on policy for trading tax doesn’t matter.